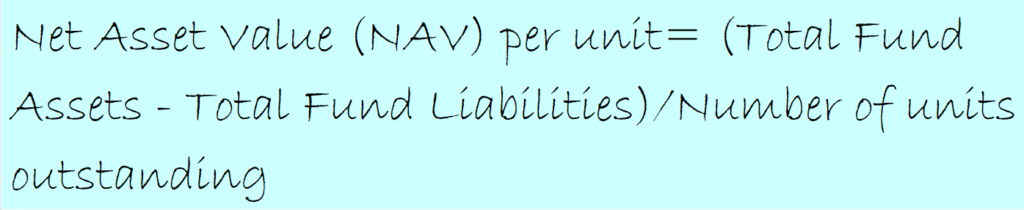

Net Asset Value (NAV) is total assets less total liabilities divided by number of shares. It is one of the most widely used terms in the mutual fund industry.

Understanding NAV for Mutual Funds

- The Total Fund Assets would typically include the mutual funds investments like stocks, bonds, T-bills, accrued income on these investments, cash and bank balances and receivables.

- The Total Fund Liabilities would typically comprise of fees owed to associated entities, borrowings, payables, accrued expenses like salaries and operating costs etc.

- To calculate NAV, the total fund assets and liabilities at the end of the trading day are considered.

- In India, the NAVs of all Mutual Fund schemes are declared at the end of the trading day after markets are closed, in accordance with SEBI Mutual Fund Regulations.

How to calculate NAV

Let us understand how NAV is calculated with an example. Suppose market value of securities held by a mutual fund are INR 2000. The liabilities of the mutual fund scheme are INR 500. The mutual fund issues 100 units of INR 10 each. So the NAV per unit = (2000-500)/100 = 15

NAV v/s Stock price

NAV is different from stock price. When a company is listed on the stock exchange, investors can buy its shares directly from the exchange at the trading stock price. In case of mutual fund, the investor buys units at net asset value from the mutual fund house. There is no concept of stock price in mutual fund units.

High NAV or Low NAV – which mutual fund to invest in?

NAV only affects the number of units you receive. A high NAV will give you less units of mutual fund scheme. A low NAV will give you more units of a mutual fund scheme. NAV should not be the deciding factor while choosing a mutual fund scheme to invest your money. The investor should look at the fund’s performance or returns generated over the years to make a decision on the investment. Let us understand this with an example.

Vinita wants to invest Rs 10,000 in a mutual fund scheme. She wants to choose between two fund schemes – A and B. The NAV of mutual fund A is Rs 200. If Vinita invests, Rs 10,000 in fund A she will get 50 units of fund A (10,000/200). The NAV of mutual fund B is Rs 500. If Vinita, puts her money in fund B she will get 20 units of fund B (10,000/500).

Suppose both funds fetch a return of 14% in one year. The market value of her investment (irrespective of fund A or fund B) would be Rs 11,400 [i.e. 10,000*14%+10,000]. Assuming no change in the NAV, if Vinita invested in fund A she would have 57 units of the fund (11,400/200). Whereas if Vinita invested in fund B she would have 22.8 units of the fund (11,400/500).

So NAV should not govern or influence your investment decision when it comes to choosing a mutual fund. Investors should look at the performance or returns that the fund has generated over the years.

{kind=link}